Published March 8, 2020

Mortgage Rates Hit Marks Never Seen Before

I made a post about

mortgage rates back on February 21st noting at the time that

mortgage rates were hovering around all time low marks. At that time I noted

that I thought there was potential for them to go lower if the corona virus

escalated, particularly in the U.S.

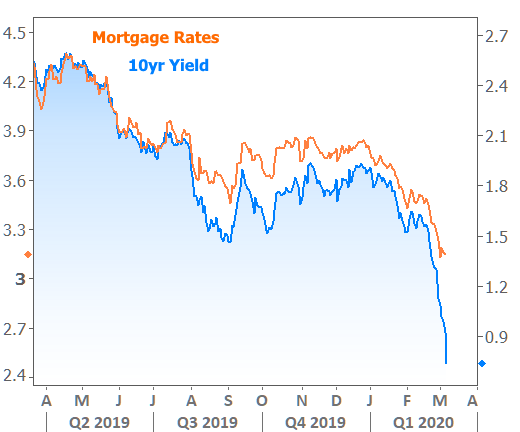

Since I made that post that’s exactly what’s happened and interest rates

have dropped to figures I’ve never seen in my 15 years in the industry.

The corona virus has

brought chaos to financial markets like few other things have. The fallout

around it is unprecedented and unlike we’ve seen before. This is particularly

true for interest rates and the mortgage market. In many ways, things are more chaotic now

than they were in 2008 but in a different way. Mortgage rates, which are tied

to the yield on the 10 Year Treasury Bond, typically track with the stock

market as it rises and falls. However

over the past week the yield on the 10 Year Treasury has plummeted nearly in

half from where it was at the start of February as investors across the world

seek safety for their money even if it means little to no return.

The day after I made

that post on the 21st the stock market began to experience some serious drops

and on Friday February 28th it bottomed out to a recent low after

some of the largest daily point losses in history. Interest rates started dropping along with

the market and the yield on the 10 Year Treasury. February 28th is the first time I’d

ever seen a 30 Year Fixed Conventional loan show up on a mortgage rate sheet offered

at 2.875% with only a small loan discount cost!

Rates on 5 Year ARM’s and 15 Year Fixed are low as well but there’s not

as much of a drop between them and a 30 Year Fixed as we typically see. That’s because the 30 Year Fixed is so ridiculously

low right now!

The market went back

up on Monday March 2nd and throughout this past week it’s bounced

around between gains and losses, and interest rates have followed in concert. Some

days we will have multiple re-prices as rates go up with the market and other

days it goes the other direction. Although the rates/pricing haven’t been as

good as they were on Friday the 28th, they are still in uncharted

territory hovering around the 3% mark for well qualified borrowers on purchases

and rate/term refinances for standard conventional loans. High balance conventional

loans ($510k-$740k) are also fantastic and just slightly above the rates for

conventional loans.

That’s enabling

borrowers who were already sitting in great loans in the upper 3’s to consider

a refinance. The question they all

borrowers should ask on a rate/term refinance is what are the costs of

refinancing, how much will I save on my monthly payment, how long will it take

for me to make up the loan costs with the savings and will I still have the

property and loan past that point. I’ve

ran those numbers for multiple people during the past week and many are seeing

that they’d make up the costs in a year or less of having the loan. If you’re

holding the property past that you’re going to get to enjoy that low rate for

the remaining time that you do. You

could also consider continuing to pay or occasionally paying the amount you

have been thereby quicker reducing your principal balance, interest generated

and time to pay-off the mortgage.

Some borrowers are taking

this opportunity to move into shorter term loans such as 15, 20 or 25 Year

amortization which in combination with the low rates may result in little or no

change in payment. Each borrowers situation is different and considering

refinancing requires having a mortgage professional reviewing it with you and

giving you input on what would best for your specific scenario.

Buyers who are in the

midst of this highly active market in the Seattle area are excited about the

opportunity that these mortgage rates are providing. The lower rates mean

either lower payments for the property you want or the opportunity to qualify

or purchase a higher priced property.

The challenge can be finding that property right now but once you do you’ll

be assured to have the potential to lock in some of the lowest interest rates

ever seen to complete your purchase.

Depending on the lending/funding source being used there may also be the

potential to float down to a lower rate than you lock in at if the rates and

pricing improve. Each of my funding sources handle that a bit differently but

all have options for it.

One element that everyone

getting a home loan right now needs to be aware of is that the industry is

getting flooded with applications. Being able to complete the process including

an appraisal in 30 days or less is going to be next to impossible. I’m locking all borrowers on purchases for 45

days and refinances and 60 days with the expectation that underwriting turn

times will be slower than normal and appraisers will be so busy that it may

take a week or two to get an appraisal done. We’ve experienced this in the past

when rates have been really low so I’m preparing all my clients to expect it if

they are going to be getting a mortgage in the near future.

As we start this week

I’m not sure what exactly to expect as we saw the market bounce up and down

over the past week. I do think that we

may not have seen the end of the large stock market drops as it seems that the

fears around the corona virus are not going away and seem likely to get worse

rather than better. If that continues to

push the market down and yields on 10 Year Treasuries go lower we may see the

interest rates get even lower. It’s also

possible that mortgage lenders hold them in this same range to slow up what’s

likely to be an onslaught of refinancing. What I can know for certain is that

we are in a really unusual time for home loans where some opportunities are

around for people to access interest rates that we’d never even considered to

be possible in the past. If you’re

curious about what options you may have to take advantage of these low rates

please reach out to me via phone, text or email and I’m happy to discuss them

with you.

Michael Pollock

| Northwest Premier Brokers

or another way