The Home Loan Process

Our Partnerships Will Make The Financing Process Easier

If you haven’t experienced it before, the home loan process can feel overwhelming, but our brokers will help you throughout the process, from pre-approval to closing. The first thing to do is get connected with a loan originator and get qualified. If you don’t already have someone in mind, we partner with one of the best financing sources in the industry, and we’d be happy to introduce you, so you’ll be well taken care of.

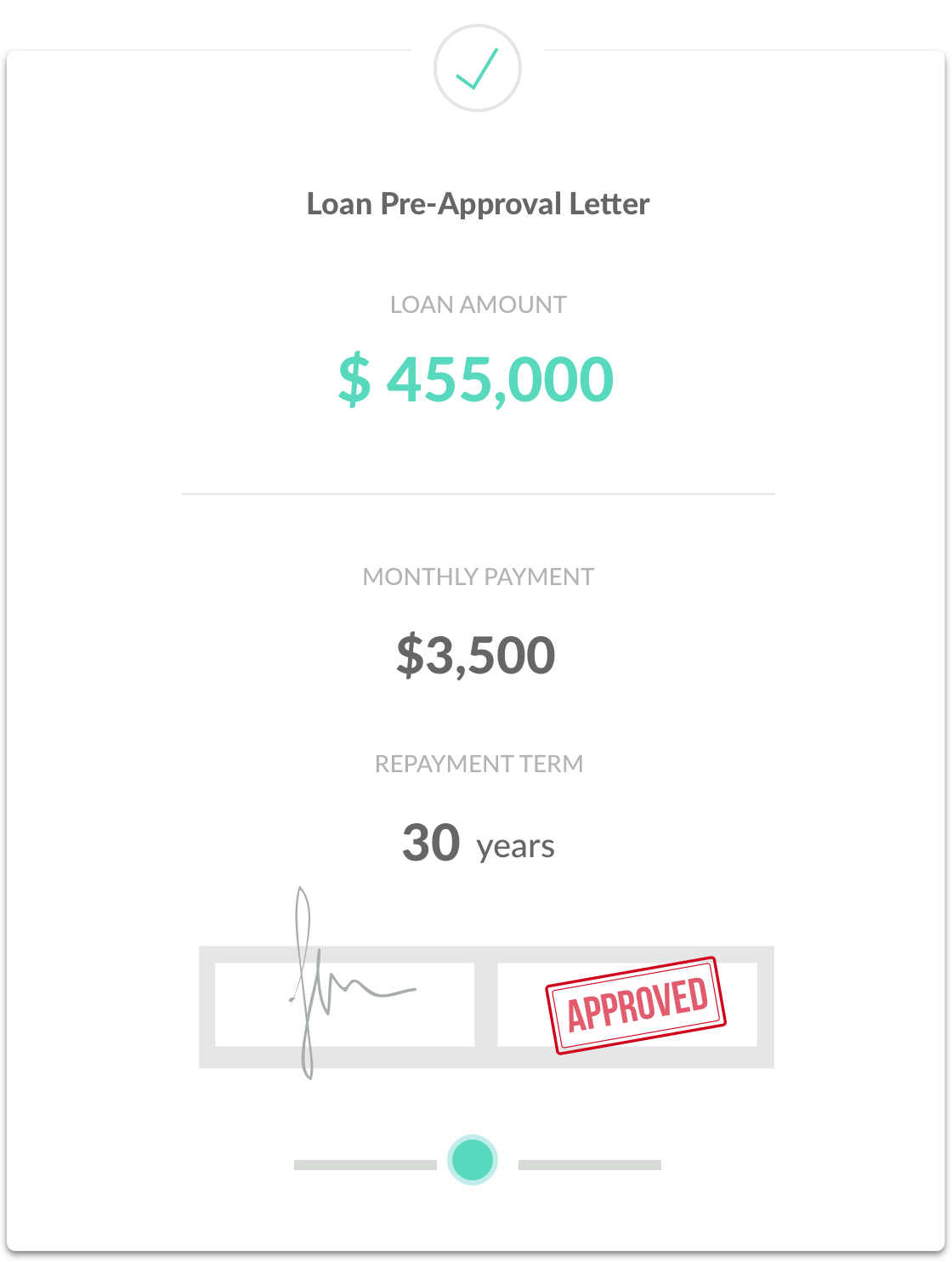

Get Pre-Approval

Before you start looking for a home to buy, it is essential to meet with a licensed loan originator to get pre-approved for financing. To get started, the originator gathers information about income, assets and debts to determine how much of a loan amount and purchase price you may be able to qualify for. The documentation needed to do this includes a credit report, W-2 forms, pay stubs, recent bank statements and potentially tax returns.

There are a variety of different loan programs, and the originator will work with you to determine the specific programs that best suit your needs and situation. Your originator will help you complete a full mortgage loan application, and talk you through the various fees and down payment options. After completing the application the originator will complete electronic underwriting on your file so they will be able to issue a financing pre-approval letter based upon a maximum purchase price.

We Will Help You Get The Best Loan

Start The Process

We’ll help you find the best local loan officer to get you fantastic interest rates and the programs that best fit your individual needs. Fill out this form and we’ll connect you with one of our lending partners today.

Application & Processing

What happens in the loan process

After you have been pre-qualified for financing and are ready to make an offer on a property what happens next? Once you find property you’re ready to buy your loan originator will issue you a financing pre-approval letter to submit with your offer. After the purchase agreement is mutually accepted the originator will setup an application for the specific terms of the purchase. The full application is submitted to underwriting, where the documents and details are reviewed by an underwriter and approves the loan if it meets compliance guidelines.

Once the underwriting approval is issued it will typically include a set of loan conditions - items that must be completed before closing can occur. The originator or processor will order appraisals and a title examination and will go over the loan conditions that will require your involvement. Once you supply the requested elements those will be reviewed and cleared by the loan underwriter.

Closing

Finalizing the loan and closing

Don’t be surprised if you’re asked for additional documentation or clarification throughout the process. That's typical and all borrowers have to work through those steps in the loan condition process. Once your loan has reached final approval by underwriting it will now be clear to close. The final loan documents will be sent to the escrow company, where you’ll sign the paperwork and pay the required amount needed for closing the transaction. After the loan and deed transfer is recorded you will be closed and ready to get the keys. Congratulations on being a new homeowner!